Posted by Debbi Kuhne on Thu, Sep 23, 2010 @ 08:32 AM

Many years ago OSHA issued a list of 14 items that qualify as First Aid. If the incident required only the First Aid treatment, the case did not need to be recorded. Yet I still see commercial contractors that are listing everything on their OSHA Logs. Just because an employee visits the occupational health clinic for a workers compensation claim, does not make it an OSHA recordable case!

The 14 items that OSHA considers First Aid are:

The 14 items that OSHA considers First Aid are:

1. Using non-prescription medications at non-prescription strength (i.e. over the counter Motrin)

2. Administering tetanus immunizations

3. Cleaning, flushing or soaking wounds on the skin surface

4. Using wound coverings, such as bandages, gauze pads, butterfly bandages, etc.

5. Using hot or cold therapy

6. Using any totally non-rigid means of support, such as elastic bandages or wraps

7. Using temporary immobilization devises while transporting injured employee (splints, slings, neck collars)

8. Drilling a fingernail or toenail to relieve pressure, or draining fluids from blisters

9. Using simple irrigation or a cotton swab to remove foreign bodies not embedded in or adhered to eye

10. Using eye patches

11. Using irrigation, tweezers, cotton swab or other simple means to remove splinters or foreign material from areas other than the eye

12. Using finger guards

13. Using massages

14. Drinking fluids to relieve heat stress

So, before just adding another case to your OSHA Log, check to make sure it is really a recordable incident. If you really aren’t sure whether to enter a case on your Log or not check it out at www.osha.gov and click on R for Recordkeeping. This will take you through the steps to determine if a case is recordable or not!

We also know a couple of great risk advisors that can also help you sort out your OSHA recordables ;)

Posted by Debbi Kuhne on Wed, Jul 28, 2010 @ 09:36 AM

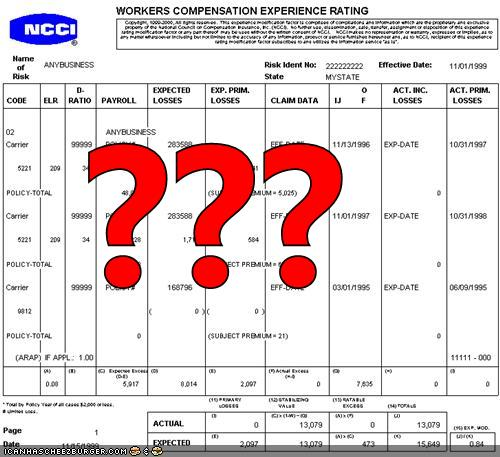

Totally confused about how your experience mod was developed? Trying to weed through formulas can be daunting and really unnecessary for the employer(you!) to understand the basics of how the experience mod is developed.

Totally confused about how your experience mod was developed? Trying to weed through formulas can be daunting and really unnecessary for the employer(you!) to understand the basics of how the experience mod is developed.

NCCI (National Council on Compensation Insurance) collects data from your Construction Insurance Carrier. This data consists of audited payroll for the 3 years prior to your current year, as well as claim amounts for the same time period. The claim amounts are incurred dollars (reserves plus amounts paid).

NCCI develops expected loss rates for each WC classification each January 1st. The rate is multiplied times your payroll and the final amount or expected loss amount is compared to your actual claim dollars. If your actual claim dollars exceed the expected your mod is in excess of 1.00, or a debit mod. If your actual claim dollars are less than the expected loss amount your mod is below 1.00, or is referred to as a credit mod.

In today’s economy many employers are reducing their workforce and thus payrolls are decreasing. If you maintain the same amount of incurred losses, but payrolls are reduced and therefore expected losses are reduced you will be seeing an increase in your mod. Unfortunately, many employers had that happen in 2010. We hope to see a stablizing of the expected loss rates in 2011, but since NCCI does not release those until December, it's anyones guess!

There are many more intricate parts to the actual calculation, but as long as you know the basic of “expected losses versus actual incurred losses” you should have a better understanding of the calculation.

If you're a Connecticut construction firm that needs experience mod help; whether it means reducing claims or making a plan to get your experience mod back down to below 1.00, Construction Risk Advisors can help. Our two full-time, in house claim advisors spend a combined 100 hours a week helping our construction clients achieve their minimum experience mod and in doing so achieve the best workers comp insurance rates possible. Give us a call at 800-252-9864 or drop us a line if you want to see how low your mod can go!

Posted by Debbi Kuhne on Mon, Jul 26, 2010 @ 03:35 PM

If I’ve heard it once I’ve heard it a hundred times --- “he wasn’t hurt that bad – he should be back at work” or “he must not really have been hurt at work”! Many employers feel a substantial number of claims are fraudulent, but statistics show that this isn’t the case. The problem is malingering after the injury occurs; it is much more prevalent, but also can be controlled.

Malingering can occur for many reasons. First and foremost is that if the treating physician or Occupational Health Clinic doesn’t have a copy of the construction workers’ job description, then they can only go by what the injured worker tells them. The injured worker can embellish their job as much as they want because there is nothing concrete to back it up. So, one way to combat malingering is to have job descriptions that you can easily provide to the Dr. or other medical provider. Another issue is that not all providers understand the importance of returning someone to work, to their regular routine, so it’s beneficial for you to have an established relationship with a local Occupational Health clinic that understands the work your construction firm does and understands you want your injured workers back on the jobsite as soon as possible!

Malingering can occur for many reasons. First and foremost is that if the treating physician or Occupational Health Clinic doesn’t have a copy of the construction workers’ job description, then they can only go by what the injured worker tells them. The injured worker can embellish their job as much as they want because there is nothing concrete to back it up. So, one way to combat malingering is to have job descriptions that you can easily provide to the Dr. or other medical provider. Another issue is that not all providers understand the importance of returning someone to work, to their regular routine, so it’s beneficial for you to have an established relationship with a local Occupational Health clinic that understands the work your construction firm does and understands you want your injured workers back on the jobsite as soon as possible!

But there are reasons that the injured worker may be malingering that have nothing to do with the injury itself. Is it possible that the injured worker was having issues with a co-worker, construction foreman, supervisor, or another subcontractor prior to the incident, and is now looking for ways to avoid returning to work?

If you suspect there is a reason the injured worker is malingering, you should be telling the claim adjuster! The adjusters at the insurance carrier do have to work within the confines of the State statutes, but they are experienced enough to know a “malingerer” when they see one and appreciate any insight you may be able to give .

So the next time there is a delay in getting your injured worker back to work, don’t jump to the idea that the whole claim was fraudulent, discuss your concerns with the claim adjuster, give them some insight into the employee and hopefully another “malingerer” will be returned to work!