Posted by Dan Phelan on Fri, Apr 29, 2011 @ 09:41 AM

What is a waiver of subrogation? You've seen this in construction contracts, on certificates, and many of your insurance policies have it, what what exactly is a Waiver of Subrogation and what does it do? A waiver of subrogation, also known as a "transfer of rights of recovery" is a mechanism that insurers use to transfer risk and to limit the rights of recovery from another party on behalf of the insured. Confused? An example of how a "Waiver of Subrogation" would work in a workers' comp claim scenario is this:

What is a waiver of subrogation? You've seen this in construction contracts, on certificates, and many of your insurance policies have it, what what exactly is a Waiver of Subrogation and what does it do? A waiver of subrogation, also known as a "transfer of rights of recovery" is a mechanism that insurers use to transfer risk and to limit the rights of recovery from another party on behalf of the insured. Confused? An example of how a "Waiver of Subrogation" would work in a workers' comp claim scenario is this:

A laborer at ABC HVAC is on XYZ General Contracting's site. ABC's laborer is injured because a piece of wood wasn't cleaned up by one of XYZ's workers. ABC's injured worker collects workers compensation for his injury, but because a waiver of subrogation was in place, ABC's insurance carrier can not go after XYZ's insurance limits to get the money they spent on the claim due to XYZ's negligence in maintaining the job site. Because ABC’s worker was injured, and ABC’s insurance carrier is on the hook for 100% of the medical and indemnity costs of the claim, ABC HVAC’s experience modification factor will increase, as well their workers compensation costs for the next three years. Depending on what ABC’s experience mod was prior to the claim, this spike could also hurt their ability to bid jobs requiring an experience mod lower than 1.00.

If a waiver of subrogation were not in place, ABC's insurance carrier could have subrogated back to XYZ's insurance carrier and make them pay the percentage of the claim that they were responsible for. This would have minimized the expense costs for ABC’s workers comp carrier, as well as minimized the effect that the claim had on ABC’s experience mod.

A popular misconception by many upstream contractors is that they are insulating themselves from liability downstream by requiring their subcontractors to provide a waiver of subrogation in their favor. While they are insulating themselves from the workers compensation insurance carriers of their subs, they are not insulated from having a suit brought by the injured worker and his/her family. Also, depending on the level of negligence by the upstream party, their general liability policy could be called upon to pay both defense costs as well as a settlement.

One last thing to consider about risk management and waivers of subrogation. There are two ways to obtain this coverage endorsement. It can be added to your policy for an annual fee, or can be obtained on a one off basis whenever required by contract. We advise our clients to have it built into their policy so that there isn't a possibility that they are in breach of contract by forgetting to have it endorsed separately for every job requiring it.

Want to get technical? Great article on IRMI.com about WOS here

If you missed our post about it last week, this blog as well as many others related to construction and contracting are available on Mike Rowe's Trades Hub.

Do you love workers compensation as much as we do? Here's the rest of our blog posts about it!

Have a question about your construction risk management program that we haven't answered on the blog yet? Ask a Risk Advisor!

Posted by Dan Phelan on Mon, Oct 25, 2010 @ 09:18 AM

Read the full NCCI Report Here

Last month NCCI (National Council on Compensation Insurance) released a report that stated while claim frequency is down, indemnity (time out of work) and severity (cost of medical treatment) are both up. This trend of claim frequency has been headed in a positive direction since 1991 due in large part to companies taking loss control and claim prevention seriously, as well as many factories and manufacturing plants adding increase automation in lieu of human workers for dangerous jobs. There has also been a marked decrease in industries like construction and manufacturing since the "recession" began in 2008. Less people working=less injuries. However, the double-edged sword to this report are that the injuries that are still occurring have become more severe. Due to the severity of some of these injuries, insurance carriers are still paying out substantial medical dollars and indemnity payments to out of work employees.

What does this mean for Connecticut construction companies? Simply, you can expect your workers compensation insurance premium to increase in 2011 through no real fault of your own. Because of the losses from your peers in your industry, your MOD may decrease up a few points on 1/1/2011. If you haven't heard from your agent what they've projected your MOD to be next year, now would be a good time to check. Especially if you're a contractor that needs a sub 1.00 MOD to bid projects. In situations like this, having an experience MOD under 1.00 is good, but not great because of its susceptibility to go over 1.00 when NCCI adjusts its rating formula. Having MODs drop a few points can be helpful if you're hovering around 1.00, but the double edged sword to this is that with the rate increase, it could cancel out the potential premium decrease from your MOD dropping.

What would be great is if you had already partnered with an insurance broker that helps contractors develop strategies to achieve their minimum mod. Not only will you not have to worry about bidding jobs, but you will also get to enjoy best in class pricing for your workers compensation insurance and have your account be looked upon favorably when it slides across the desk of an insurance company underwriter. A couple of other bonuses for contractors that maintain a MOD below 1.00 is that they can apply for the Connecticut Contractor Credit on their workers comp insurance (less premium!) as well as receiving a credit for having a "credit MOD". As a caveat, these credits aren't available from every insurance carrier (some carriers can provide cheap quotes without using credits because they don't actually understand how construction insuranace works).

So to sum it up:

Losses are down, but the cost per claim is up.

Because claim costs are up, NCCI is going to have to adjust their calculations. Early predictions is a rise in MODS for all experience mod rated companies.

Talk to you agent about your mod. Find out what they predict it will be in 2011. If it's going to be around .97-1.00, try to put a plan in place ASAP to lower reserves and close claims.

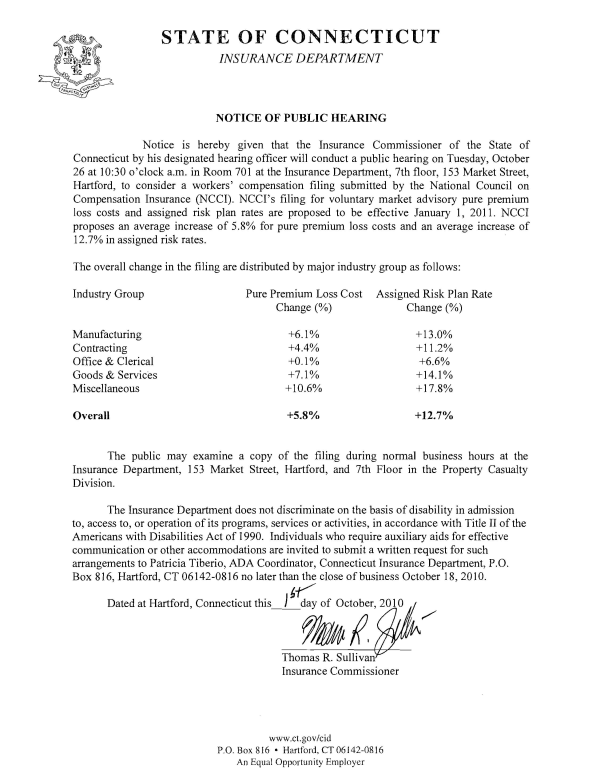

Tomorrow in Hartford, there will be a public hearing explaining the change in NCCI's rating. Details here

Posted by Robert Phelan on Wed, Oct 20, 2010 @ 02:13 PM

Measuring the “Cost of Ownership” of Construction Insurance

We have written posts about the Total Cost of Risk and I suspect many construction company owners don’t relate to that concept. So I’m going to try another angle.

Many of you make large capital equipment purchases throughout the year. Let’s use an Excavator as an example. In addition to the standard comparison items like:

Track length

Reach

Dig Depth

Lift Capacity

Operating Weight

You are also going to look at Cost of Ownership. This would include items such as:

Can I depend on this Mfr/Model to be free of expensive maintenance?

What are the annual operating expenses?

How strong is the warranty?

How about trade in value? Does this make/model hold it’s value?

What kind of downtime will I have for standard maintenance?

In other words, what does it cost to own this piece of contracting equipment?

Connecticut contractors need to look at insurance purchasing the same way. Just as in equipment, the premium does not reflect the total cost of ownership. Two pieces of equipment that have the same price tag could have very different costs of ownership.

What are the kinds of comparison points that you would look at when evaluating insurance?

First would be considerations of your Risk Advisor or Insurance Agent. You would compare:

Experience of the service team:

Breadth of capabilities (Safety consulting, Claim consulting, HR assistance, Bid spec review, Contract terms evaluation, etc.)

Willingness to receive performance-based compensation

Workers Comp Experience Mod Rate improvement plan

Problem solving abilities

Second would be the insurance carriers:

Which ones specialize in contractors of your type?

What specialized services do they have for contractors?

What is the average tenure of their claim reps?

Do they have a Preferred Provider Network that works for you?

Are their loss control reps construction specialists?

Are their in-house lawyers construction specialists?

These services are about two things: Preventing claims and minimizing the expenses of claims you have (The TRUE Cost of Risk). If one construction workers comp claim is mismanaged, it could not only cost you lots of time and money. It could cost you work. Every Connecticut contractor insurance buyer knows that an EMR of 1.0 or greater puts them in the “danger zone” of not only an increase in construction workers compensation premiums, but also in their ability to bid jobs for certain owners and general contractors.

What would the cost be to your construction company if you couldn’t bid or didn’t get $2M worth of work in the next three years? Will the broker/carrier combination you have just chosen based on a low bid be the best ones to prevent this from happening? Think of that carefully and be sure to pay as much attention to insurance buying as you do to equipment buying.

Posted by Debbi Kuhne on Wed, Jul 28, 2010 @ 09:36 AM

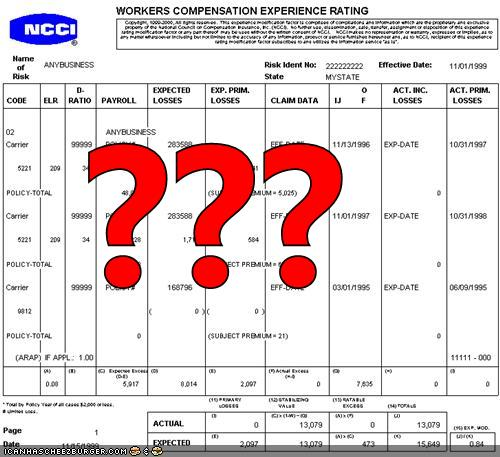

Totally confused about how your experience mod was developed? Trying to weed through formulas can be daunting and really unnecessary for the employer(you!) to understand the basics of how the experience mod is developed.

Totally confused about how your experience mod was developed? Trying to weed through formulas can be daunting and really unnecessary for the employer(you!) to understand the basics of how the experience mod is developed.

NCCI (National Council on Compensation Insurance) collects data from your Construction Insurance Carrier. This data consists of audited payroll for the 3 years prior to your current year, as well as claim amounts for the same time period. The claim amounts are incurred dollars (reserves plus amounts paid).

NCCI develops expected loss rates for each WC classification each January 1st. The rate is multiplied times your payroll and the final amount or expected loss amount is compared to your actual claim dollars. If your actual claim dollars exceed the expected your mod is in excess of 1.00, or a debit mod. If your actual claim dollars are less than the expected loss amount your mod is below 1.00, or is referred to as a credit mod.

In today’s economy many employers are reducing their workforce and thus payrolls are decreasing. If you maintain the same amount of incurred losses, but payrolls are reduced and therefore expected losses are reduced you will be seeing an increase in your mod. Unfortunately, many employers had that happen in 2010. We hope to see a stablizing of the expected loss rates in 2011, but since NCCI does not release those until December, it's anyones guess!

There are many more intricate parts to the actual calculation, but as long as you know the basic of “expected losses versus actual incurred losses” you should have a better understanding of the calculation.

If you're a Connecticut construction firm that needs experience mod help; whether it means reducing claims or making a plan to get your experience mod back down to below 1.00, Construction Risk Advisors can help. Our two full-time, in house claim advisors spend a combined 100 hours a week helping our construction clients achieve their minimum experience mod and in doing so achieve the best workers comp insurance rates possible. Give us a call at 800-252-9864 or drop us a line if you want to see how low your mod can go!

Posted by Debbi Kuhne on Thu, Jun 17, 2010 @ 10:53 AM

Is the timely reporting of workers compensation claims really that important? Absolutely! The smallest claim can turn into a 6 figure nightmare merely by not being reported promptly. A delay of just a few days can alter the outcome of a claim and raise the associated claim dollars through the roof!

Is the timely reporting of workers compensation claims really that important? Absolutely! The smallest claim can turn into a 6 figure nightmare merely by not being reported promptly. A delay of just a few days can alter the outcome of a claim and raise the associated claim dollars through the roof!

Having trouble believing this? Well, here are some reasons:

First and foremost is treatment for the injury. We have seen many "sore shoulders" go unattended only to end up with the employee seeking treatment in the middle of the night at the local Emergency Department. The charges for Emergency Room visits are easily 3 times those of an Occupational Health Clinic, so the medical costs of this incident just tripled. Emergency room providers are great at what they handle - emergencies! But they tend to handle the work related injury by automatically keeping the employee out of work an average of 3-5 days .....another increase to the cost of the claim!

Those same shoulder and soft tissue injuries that went untreated for several days, can eventually become major surgery issues, lost time claims with substantial permanency ratings, and in many cases full and final settlements. By reporting the claim immediately, the employer can and should direct the injured worker to the local occupational health clinic thus hopefully mitigating the overall cost of the claim.

An employer should never delay reporting a claim or directing the injured worker for treatment. Either of these can result in a disgruntled employee who ultimately hires an attorney. Attorney involvement on Workers' Comp claims slows down the progress of the claim resulting in increased dollars.

Insurance carriers have specific time lines in which to make payment to a claimant and meet other standards. If these are missed due to a claim being reported late, the carrier can still incur fines for not meeting required deadlines. These fines become an expense on your Workers' Comp claim!

Hopefully these are reasons enough for you to encourage your employees to report all incidents immediately and for you to report the incident to the carrier the same day. This quick response can help contain your claim dollars as well as keep your experience mod and premium lower that your competitors!

If one of your construction laborers or foremen were injured on the job, does your construction firm already have an established relationship with an Occupational Health Clinic? Did your insurance agent help you with this and provide job descriptions for the clinic to keep on file? Construction Risk Advisors has relationships with many of the occupational health clinics that treat injured Connecticut contractors every day. We can help facilitate this for your company as well as work together to prevent the claim in the first place!

Posted by Robert Phelan on Mon, Jun 07, 2010 @ 01:40 PM

One of my salespeople had a conversation today with an irate prospect. This company owner had just learned that their workers compensation experience mod rate (EMR for short) is about to go up significantly. This wasn't just going to cost more money but possible threaten this company's ability to bid work. Wouldn't you be upset, too?

You should never be surprised by a change in your workers comp experience mod. Whether your experience mod goes up or down, you should know well in advance. If you don't, then you have a problem with your insurance agent.

Unfortunately, most insurance agents think that it's YOUR experience mod so it's YOUR problem. To a point that is true. There is only so much that any outsider can do to help influence the direction of your experience modification factor and the safety procedures of a Connecticut Contractor. But why are you paying your agent a commission on that workers comp policy? Is their only job to show up once a year and say, "I'm sorry but your experience mod went up 20 points because of that loss three years ago which means your premium is up $32,000 (which means I make more money). And by the way, maybe you should hire a safety manager".

Unfortunately, most insurance agents think that it's YOUR experience mod so it's YOUR problem. To a point that is true. There is only so much that any outsider can do to help influence the direction of your experience modification factor and the safety procedures of a Connecticut Contractor. But why are you paying your agent a commission on that workers comp policy? Is their only job to show up once a year and say, "I'm sorry but your experience mod went up 20 points because of that loss three years ago which means your premium is up $32,000 (which means I make more money). And by the way, maybe you should hire a safety manager".

What's wrong with this picture? The insurance agent brings bad news. The insurance agent provides no services to help you solve the problem. The agent makes more money which you pay him as part of your premium. You suffer. That sounds like a win/win!

Forgive my sarcasm. I just can't figure out why business owners put up with this treatment. Not only will they accept this lousy service, but they'll stay with a joker like this as long as he keeps bringing them cheap insurance. If your experience mod keeps going up, you don't have cheap insurance.

Whether your experience mod is presently high or low, you should have a plan in place to improve it to its lowest possible level. You may never achieve the goal of getting your experience mod to this level, but you'll be a hell of a lot better off than your competitor who has no goal.

Last week we brought great news to a contractor client. After three years of working together, we achieved their lowest possible experience mod. When they initially signed on as a client, their experience mod was a 1.12, and by implementing our expert claims management and improving their safety program, we helped them get down to a .84!It was exhilarating for both of us. They saved a lot of money and with our help, will continue to save (around 12K annually!). We executed the plan we promised and delivered the results.

Don't let your experience mod be a mystery any longer. Work on it every day like any other goal you set for your construction firm, and you too, will celebrate success.

Are you a Connecticut Contractor that needs experience mod help? The workers compensation experts at Construction Risk Advisors are only an email or phone call away. We'd be happy to take a look at your experience mod and safety program, and offer any help we can to make you a safer and more profitable construction firm as part of our innovative Test Drive program.

Posted by Debbi Kuhne on Tue, Jun 01, 2010 @ 10:09 AM

You have heard about the benefits and cost savings if you bring an injured contractor back to modified duty. But, how can an injured worker bring any value to a construction site?

Before we examine ideas on return to work, first we need to recognize that "RTW" is beneficial for both the employee and employer. Statistics show that workers who remain in their regular routine recover quicker then those that don't! In fact, the majority of injured workers who are out of work for 12 weeks or more never return to their original jobs. The benefit to the employer? Why reduced workers comp claim costs of course and therefore, a positive impact on your experience mod and the morale of your work force!

Your employee handbook should include your "RTW" policy. This policy should clearly state that modified duty will be provided when possible, for a limited time period. The limited time period is important as you most likely do not have a modified duty position that can be a permanent position.

So, now that we have covered the benefits of returning injured workers and the importance of having a statement in your employee handbook, you are still saying "but we don't have anything for him/her to do". When it comes to modified duty you should first look at what can be temporarily changed in the worker's usual job - can someone else do the heavier lifting? But if there is absolutely no way to modify the current job, you may need to be a bit creative in providing meaningful and productive work. Is it time for an inventory review? Can the person (within their restrictions) be a safety or traffic person at the Construction Site? Do you have paperwork to be done in the jobsite trailer? Did you know that you can even pay your employee while they work at the local soup kitchen, library, or retirement home? As long as the employer is providing modified work within the medical restrictions and the employee gives their consent, the employee and the employer are both benefiting!

The next time you have an injured worker released to modified duty don't immediately say "We're a Construction Company, what can they possibly be thinking". Instead, think outside the box and help the injured worker recover quicker and help you to save workers compensation claim dollars.

The next time you have an injured worker released to modified duty don't immediately say "We're a Construction Company, what can they possibly be thinking". Instead, think outside the box and help the injured worker recover quicker and help you to save workers compensation claim dollars.

Posted by Debbi Kuhne on Mon, May 10, 2010 @ 11:47 AM

At least 50% of the

NCCI mod worksheets we review for our clients are in error. The most likely error is missing payroll. Not from your standard program but if you are a contractor engaged in OCIP(Owner Controlled Insurance Program) and CCIP(Contractor Controlled Insurance Program) jobs, that's where the errors occur!

A few years ago we had a large contractor that was hovering at a 1.00 mod - and we all know what that can mean! While verifying their mod worksheet we noted that all the payroll and Workers Comp claims under the standard program were included, but realizing a high percentage of work had been done under OCIPs and CCIPs we wondered why that wasn't reflected on the experience modification worksheet. After several months of tracking down the individual at each carrier responsible for filing the data and finally having that data provided, the mod went from 1.00 to .97!

Missing payroll is not the only error that can occur. Incorrect payroll, misclassification of construction workers, or duplication of claims also cause many, many errors. Your experience mod rate is only as good as the data that is entered into the system!

Missing payroll is not the only error that can occur. Incorrect payroll, misclassification of construction workers, or duplication of claims also cause many, many errors. Your experience mod rate is only as good as the data that is entered into the system!

So, if your mod hasn't been verified lately now is the time to do it! Who knows, you may be able to reduce your mod by several points!

Need someone to verify your experience mod? The claims team at Construction Risk Advisors has been successfully recovering misallocated premium and experience mod dollars for Connecticut contractors for a long time!

Posted by Debbi Kuhne on Thu, May 06, 2010 @ 12:51 PM

We've all heard of it - light duty, modified duty, restricted duty, and transitional duty. Regardless of what you call it, you have an injured worker who can't do their regular job and the claim adjuster is asking you to bring them back to work!

Employers and HR personnel struggle with this daily, and it seems construction companies usually have the most difficulty in developing jobs within the worker's restrictions. So should you even bother to try? The answer is absolutely Yes!

First and foremost it has been proven that keeping an injured construction worker in their normal routine (getting up, going to work, etc) helps in the recovery process. Next is the fact that by providing modified duty work you are sending the message to employees that having a work related injury does not automatically result in time off from the job. Finally, by bringing the injured worker back it is helping to reduce the claim costs and thus have a more positive effect on your experience mod.

It's a good idea to have pre-developed modified duties or jobs. We all have things we would like to accomplish, if we only had some extra time. Start keeping a running list of these and you have started your modified duty list!

So the next time the adjuster asks if you have modified duty available, don't sigh and roll your eyes - pull out your list, say yes and get that employee back to work!

Need help developing a Return to Work program for your construction firm? We can help! There are other options than just having your injured worker counting paperclips and shredding paper. Get in touch with one of the Construction Risk Advisors and we can guide you as well as help prevent the injury in the first place!

Need help developing a Return to Work program for your construction firm? We can help! There are other options than just having your injured worker counting paperclips and shredding paper. Get in touch with one of the Construction Risk Advisors and we can guide you as well as help prevent the injury in the first place!

Posted by Robert Phelan on Wed, Apr 28, 2010 @ 12:38 PM

Would Massey Energy have lost twenty-nine workers in a mining accident on April 5th if safety training was a strong cultural value? Would Toyota have recalled 2.3 million vehicles in January of 2010 if safety was of paramount concern in the design of their cars?

I think the answer to both these questions is, "No". These companies were not focused on safety and it cost people their lives.

I think the answer to both these questions is, "No". These companies were not focused on safety and it cost people their lives.

Google either one of these safety disasters and you'll get tired of hitting the "Next" button after the 10th page. In the short run, and maybe forever, both these companies have seriously tarnished their image. The public thinks company profit was more important than human lives. Who wants to be known for that?

Connecticut Contractors of all types are involved in dangerous work every day. If there was an unfortunate disaster on one of your jobsites, would your safety training practices stand up to the scrutiny of the press? How much would your reputation suffer? How long would you be on OSHA's "hit list"? How well would you be able to document your company's safety practices?

Unfortunately, many Connecticut construction firms don't consider safety training in their strategic plans. Nor do they consider the safety training capabilities of the insurance agent or insurance company they choose each year. Far too often the focus is on price and risk management is ignored.

Unfortunately, many Connecticut construction firms don't consider safety training in their strategic plans. Nor do they consider the safety training capabilities of the insurance agent or insurance company they choose each year. Far too often the focus is on price and risk management is ignored.

Who is protecting your company's reputation? Risk management is not about buying cheap insurance. If you have an insurance agent whose only focus is selling you cheap insurance, you've hired the wrong one. Don't wait to see your name in the paper before getting a risk advisor who helps make safety your highest priority.